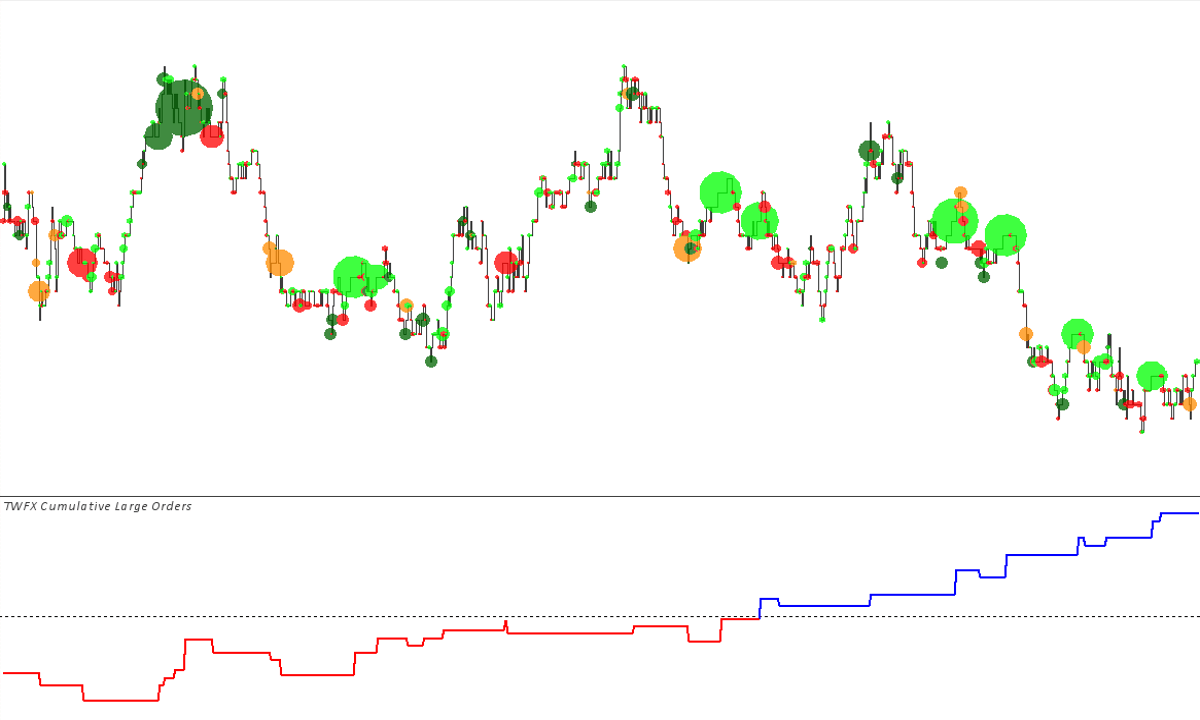

The Cumulative Large Orders Study is designed specifically to be used with the Trade Tape Chart (Main) Study, the study provides an alternative means for displaying large volume orders, as defined by the filtering mode and the Trade Tape Chart combining mode.

Note: The Cumulative Large Orders Study should not be considered to be 100% accurate in determining large orders, as they can only be inferred from market order behavior. A filter is included so that the method for counting large orders can be adjusted depending on requirements.

The study provides different methods for determining the cumulative sum and options for when it should be reset.

The study is summarised in the following update post – Reconstructed Tape Chart.

Note:

- This study can only be used on charts with a chart data type of ‘Intraday Chart‘

- It is required to use ‘Intraday Data Storage Time Unit‘ setting ‘1 Tick’

- The study is designed specifically to be used in conjunction with the TWFX Trade Tape Chart study, it will not work in any other configuration.

Inputs

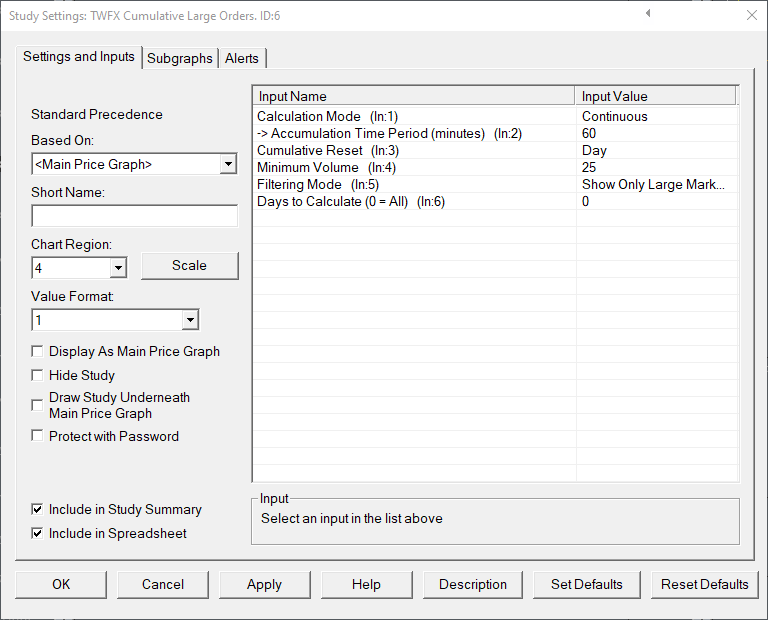

Calculation Mode (In:1)

For the purposes of the cumulative sum, Ask (Buy) Large orders are treated as positive, whereas Bid (Sell) Large orders are threated as negative.

- Continuous:

Large orders are accumulated continuously, or until it is reset at the either at the beginning of each trading day or session, as determined by the ‘Cumulative Reset’ input. - Time Period – Rolling:

Large orders are accumulated in a continuous rolling sum, covering only the most recent ‘Accumulation Time Period’, the cumulative sum may also be reset at the beginning of each trading day or session, as determined by the ‘Cumulative Reset’ input. - Time Period – Fixed:

Large orders are accumulated over a fixed time period, as determined by the ‘Accumulation Time Period’, after which it is reset to zero and the accumulation restarts. The cumulative sum may also be reset at the beginning of each trading day or session, as determined by the ‘Cumulative Reset’ input.

Accumulation Time Period (minutes) (In:2)

Defines the accumulation time period, measured in minutes, used for ‘Time Period – Rolling’ and ‘Time Period – Fixed’ calculation modes.

- Min: 1

- Max: 1440

Cumulative Reset (In:3)

Defines if / when the cumulative large order sum should be reset (in additon to any Time Period based reset).

- None:

Cumulative sum is not reset (does not apply to ‘Time Period – Fixed’ calculation mode). - Day:

Cumulative sum is reset at the beginning of each trading day, as determined by the chart session times settings. - Session:

Cumulative sum is reset at the beginning of each trading session, as determined by the chart session times settings.

Filtering Mode (In:5)

- None:

The total volume for any chart bar having met the minimum volume threshold is counted as large order volume. - Show Only Large Market Orders:

Where it is possible to determine, based on the Trade Tape Chart study configuration, large single trades having met either of the minimum volume thresholds will be counted as large orders. Where it is not possible to determine large orders across multiple price levels, the only the price level with the largest volume for a single trade will be counted as large order volume.

NOTE: For “Show Only Large Market Orders” to function correctly, the use of a Sierra Chart provided data feed is required and the “Combine Trades into Original Summary Trade” option must be enabled, refer to the following for more information – https://www.sierrachart.com/index.php?page=doc/ChartSettings.html#CombineTradesIntoOriginalSummaryTrade.

Days to Calculate (0 = All) (In:4)

Defines the number of days over which the study is calculated, can be used to reduce the initial study calculation time when many days worth of data is loaded into the chart but this study is only required to be shown on the most recent days.

- Min: 0 (in which case all loaded bars are evaluated during the study calculation)

- Max: 1000000

Subgraphs

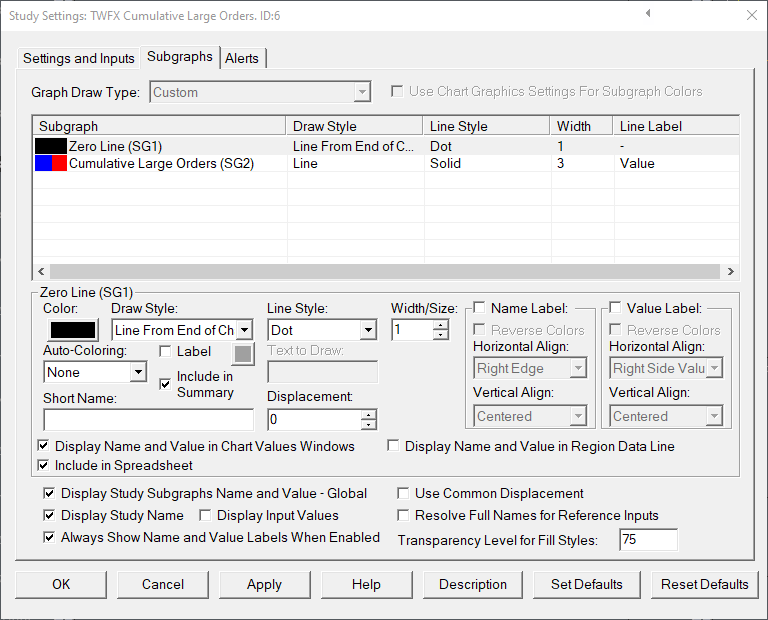

Zero Line (SG1)

Default: Line Extend to Edge

Displays horizontal axis at zero to suit zero centered subgraph display.

Cumulative Large Orders (SG2)

Default: Line

Displays the accumulated large orders